The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

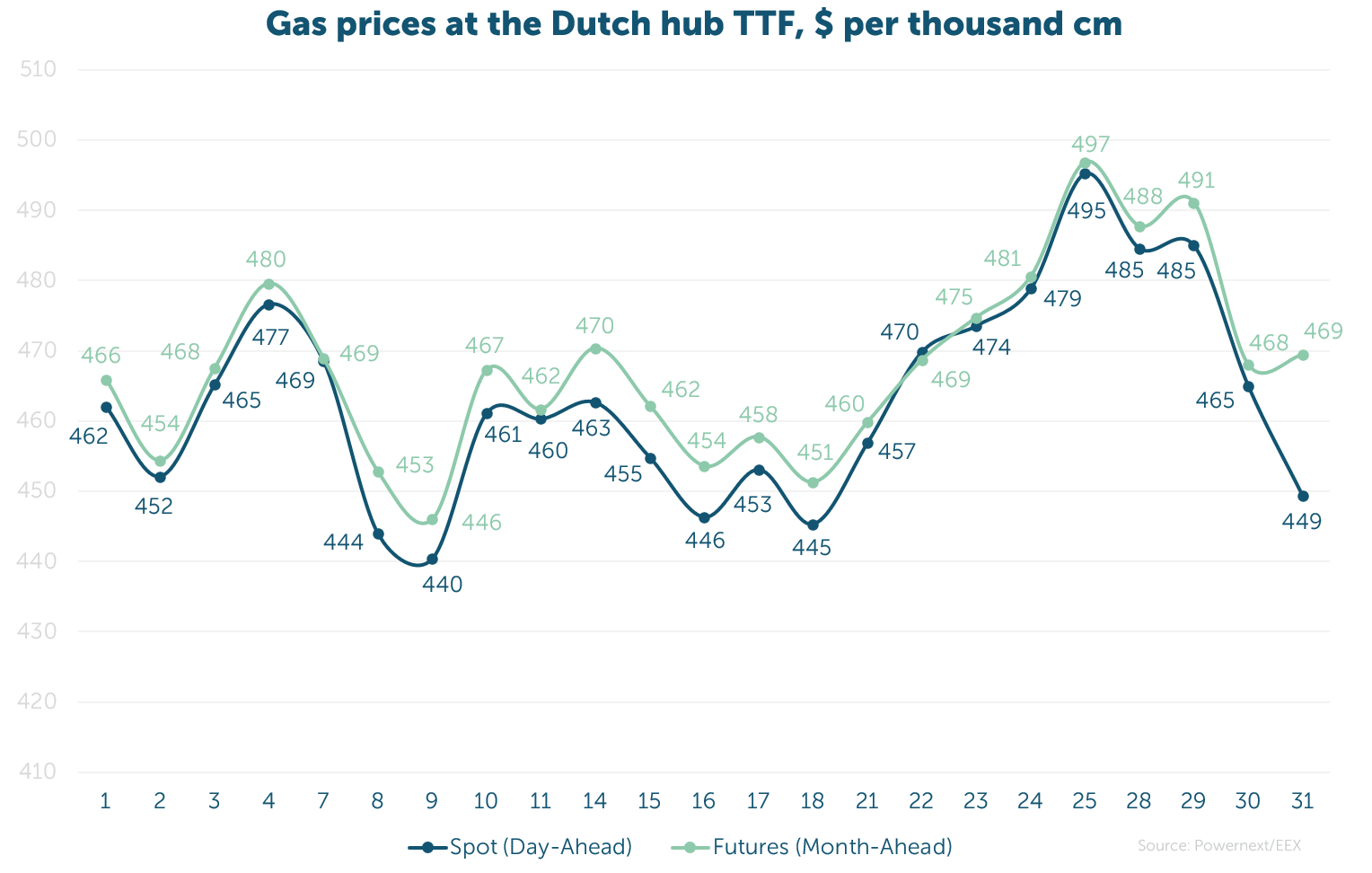

The average spot price was 40.024 EUR/MWh ($459, or UAH 18 937 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, was 40.396 EUR/MWh ($463, or UAH 19 112 per thcm).

Over the month, spot market prices rose by 10.7%, while futures prices increased by 12%. The price difference between these derivatives was 0.9%.

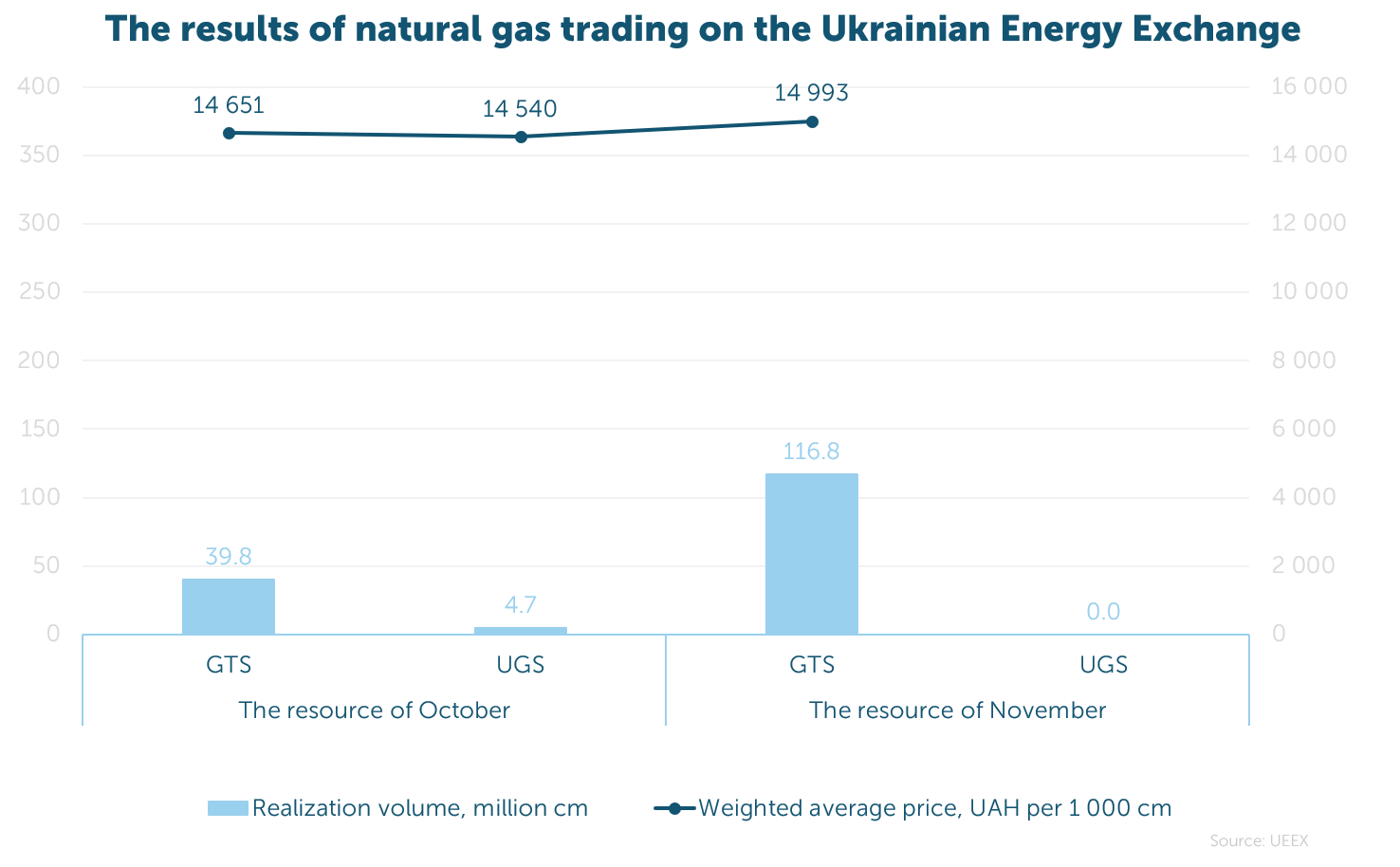

Throughout the month, 161.3 million cm of gas were sold on the exchange at a weighted average price of UAH 14 852 per thcm (net of VAT, under all payment terms in the GTS/UGS). Of this volume, 97% was traded in the GTS and 3% in the UGS.

GTSOU purchased 84 million cm, and the Naftogaz Group - 7.2 million cm. Key sellers were Ukrnafta (56.1 mcm), Ukrnaftoburinnya (11.2 mcm), and Nadra-Geoinvest (2.5 mcm).

Over ten months, a total of 1.540 bcm was traded on the UEEX, and since 2022 – 2.875 bcm (excluding GMU).

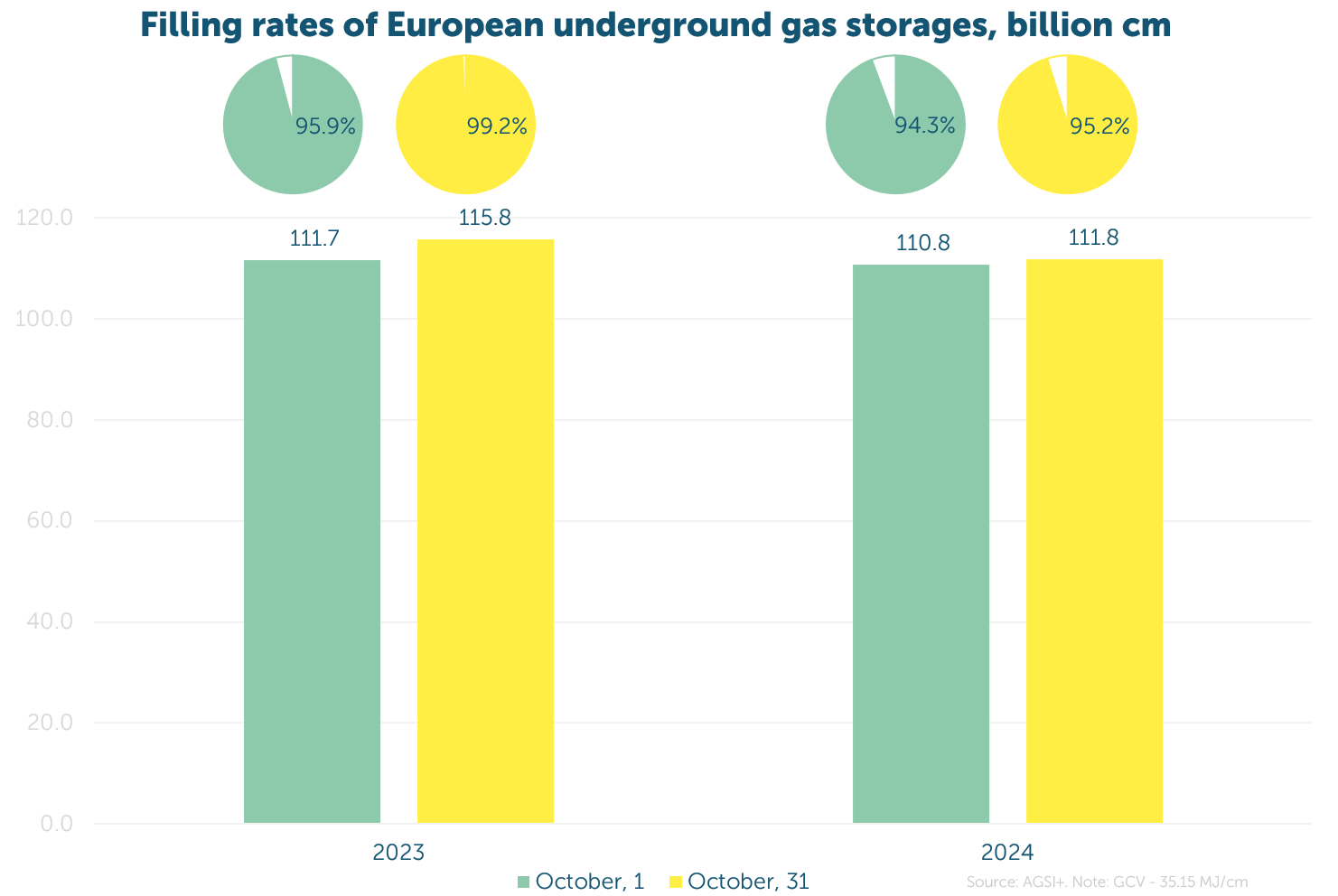

EU member countries fully met the European Commission's requirements to fill gas storages ahead of the 2024/2025 winter season, surpassing the 90% target by November 1.

According to ENTSO-G's projections, to meet the EU's target of 90% for the following winter, UGS levels should be maintained at 30-40% by the end of the heating season.

This target will be achieved through sustained moderate demand, continuous supplies from Norway, and uninterrupted LNG inflows.

In October, 338.3 million cm of gas was transported to Ukraine, a 39% increase compared to September. Of this, 84% were transported from Hungary and 16% from Slovakia.

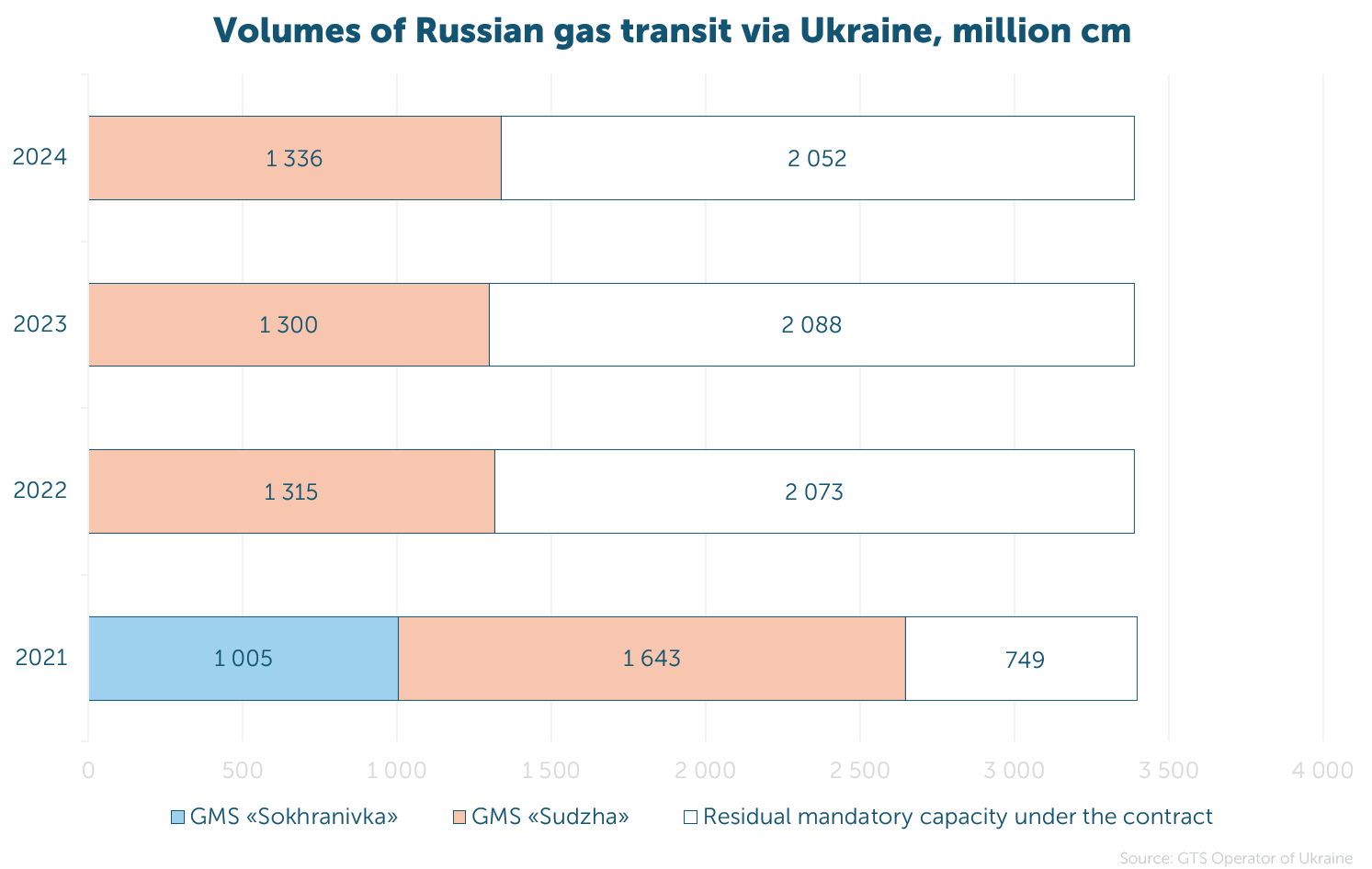

Gazprom transported 1.33 bcm in October, equating to 39% of the contracted volume, marking a 2.8% increase compared to 2023 but a 50% decrease relative to the same period in 2021.

The total transit volume for ten months amounted to 12.9 bcm, 7% more than the previous year.