The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

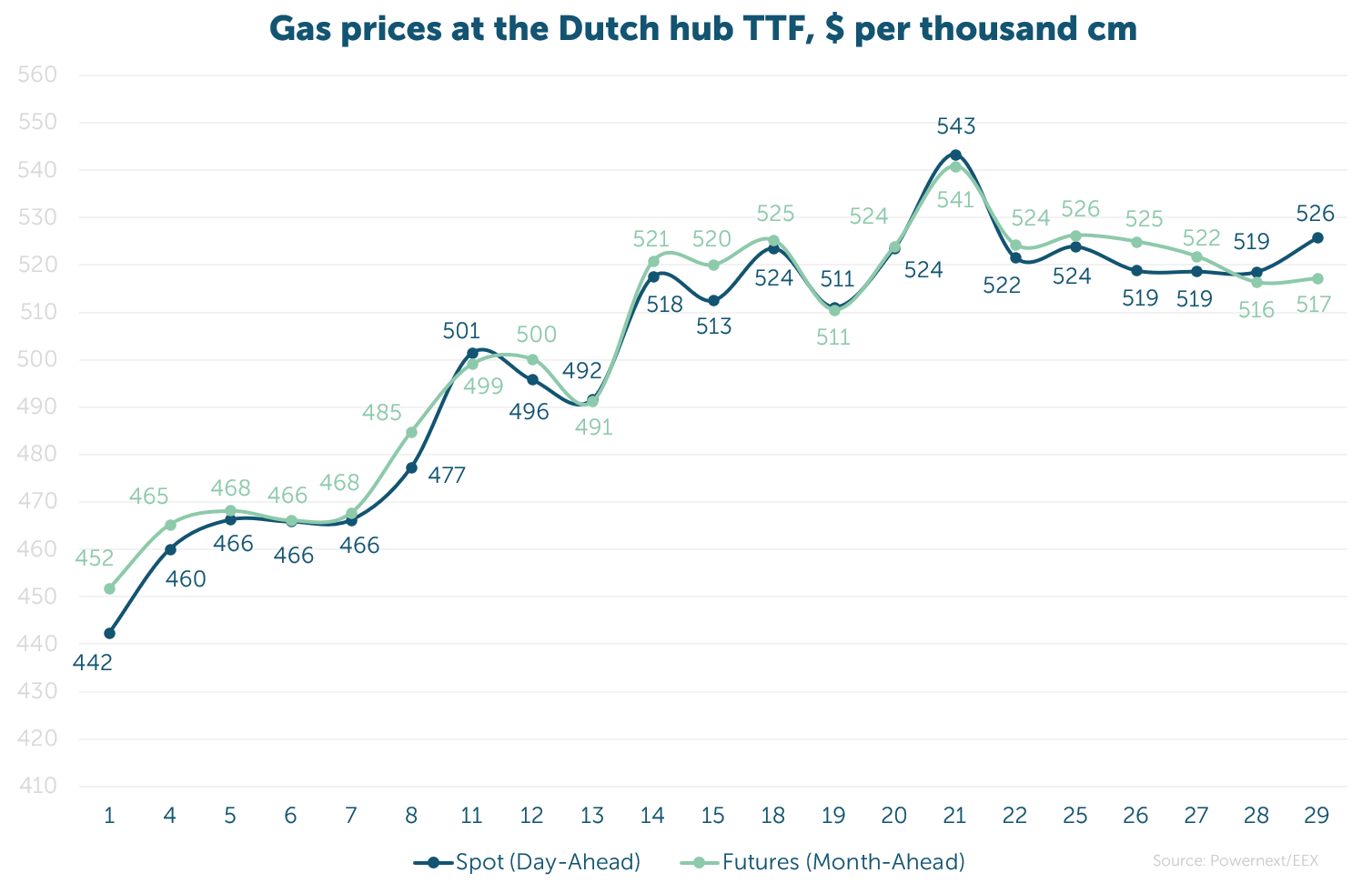

The average spot price was 44.461 EUR/MWh ($502, or UAH 20 756 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, was 44.632 EUR/MWh ($504, or UAH 20 836 per thcm).

Over the month, the spot market price increased by 11.1%, while the futures market price rose by 10.5%. The price difference between these derivatives was 0.4%.

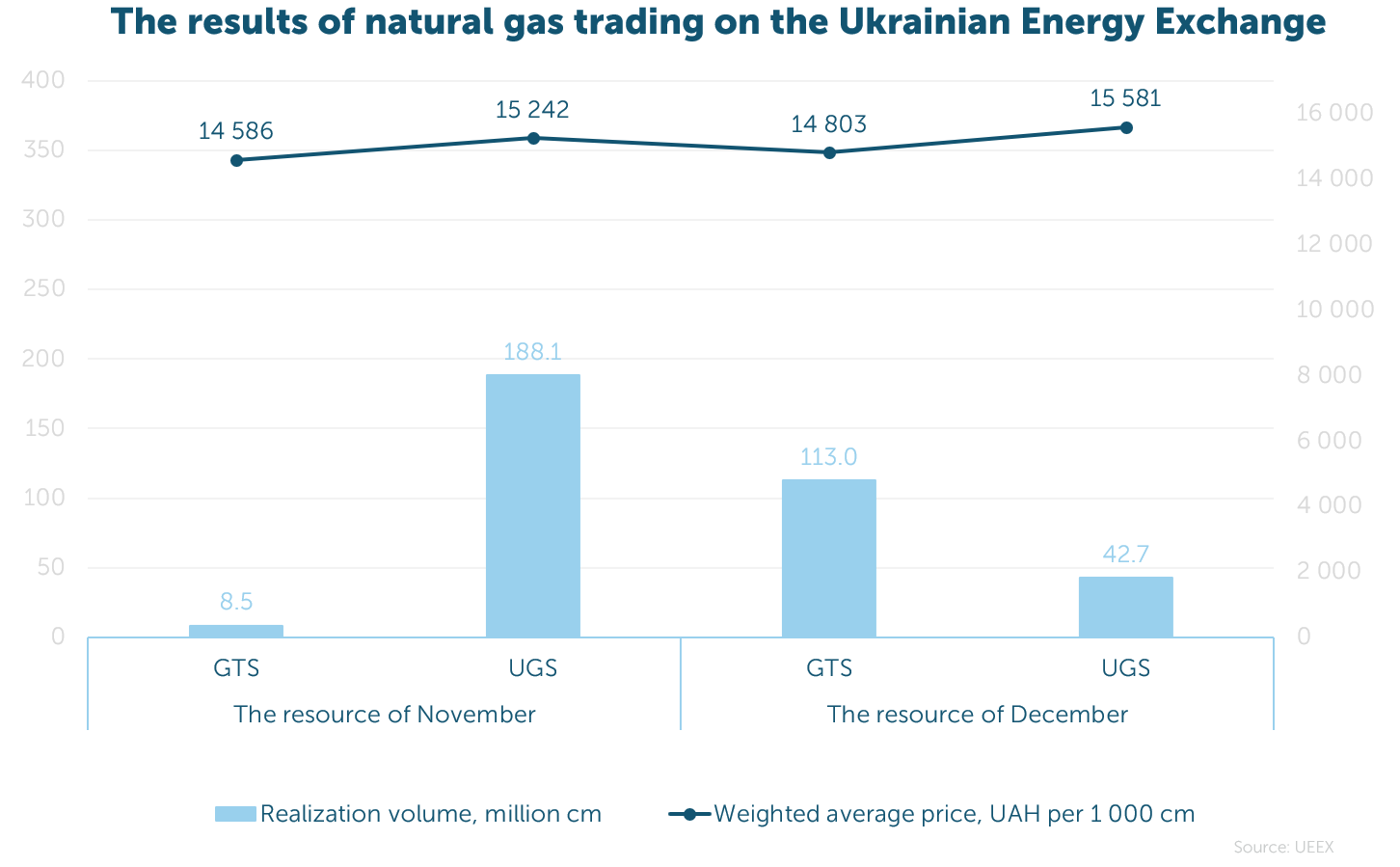

In November, 352.2 million cm of gas were sold on the exchange at a weighted average price of UAH 15 126 per thcm (net of VAT, under all payment terms in the GTS/UGS).

The lion’s share of the resource was purchased by the Naftogaz Group — 237.5 million cm, or 67%. Producers were also active: Ukrnafta sold 47.5 million cm (13%), UNB – 39.9 million cm (11%), and Nadra-Geoinvest – 5.6 million cm (2%).

Over 11 months, 1.892 bcm were sold on the UEEX, and since 2022 – 3.227 bcm (excluding GMU).

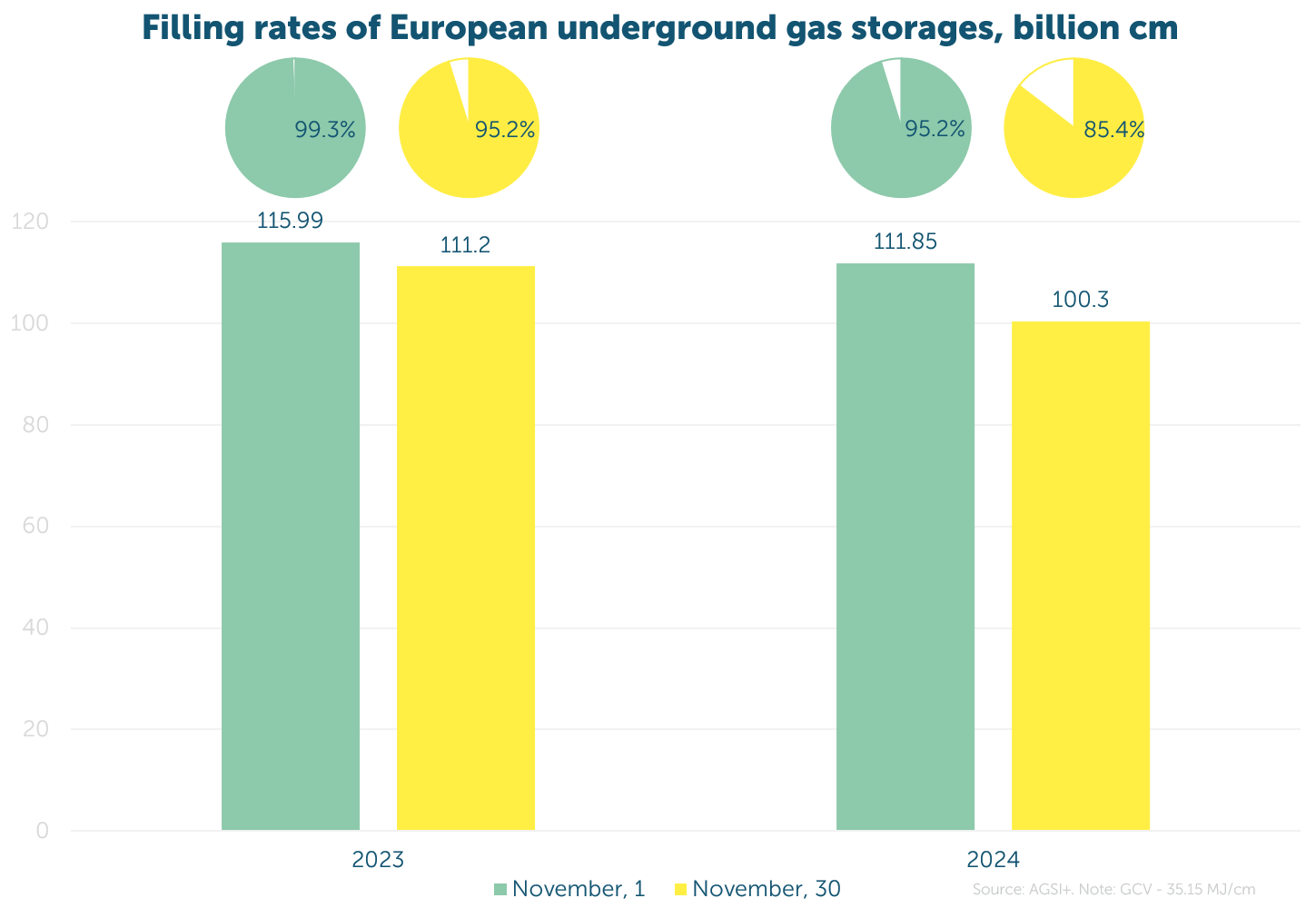

In November, Europe withdrew a record amount of gas from storages, entering winter with the lowest reserves in the past two years.

One of the key reasons was increased gas use for electricity generation, as the share of renewables declined, and the weather turned colder and less windy than previously forecasted.

Seasonal factors and the anticipated halt of Russian gas transit through Ukraine are expected to impact the European market in the coming months.

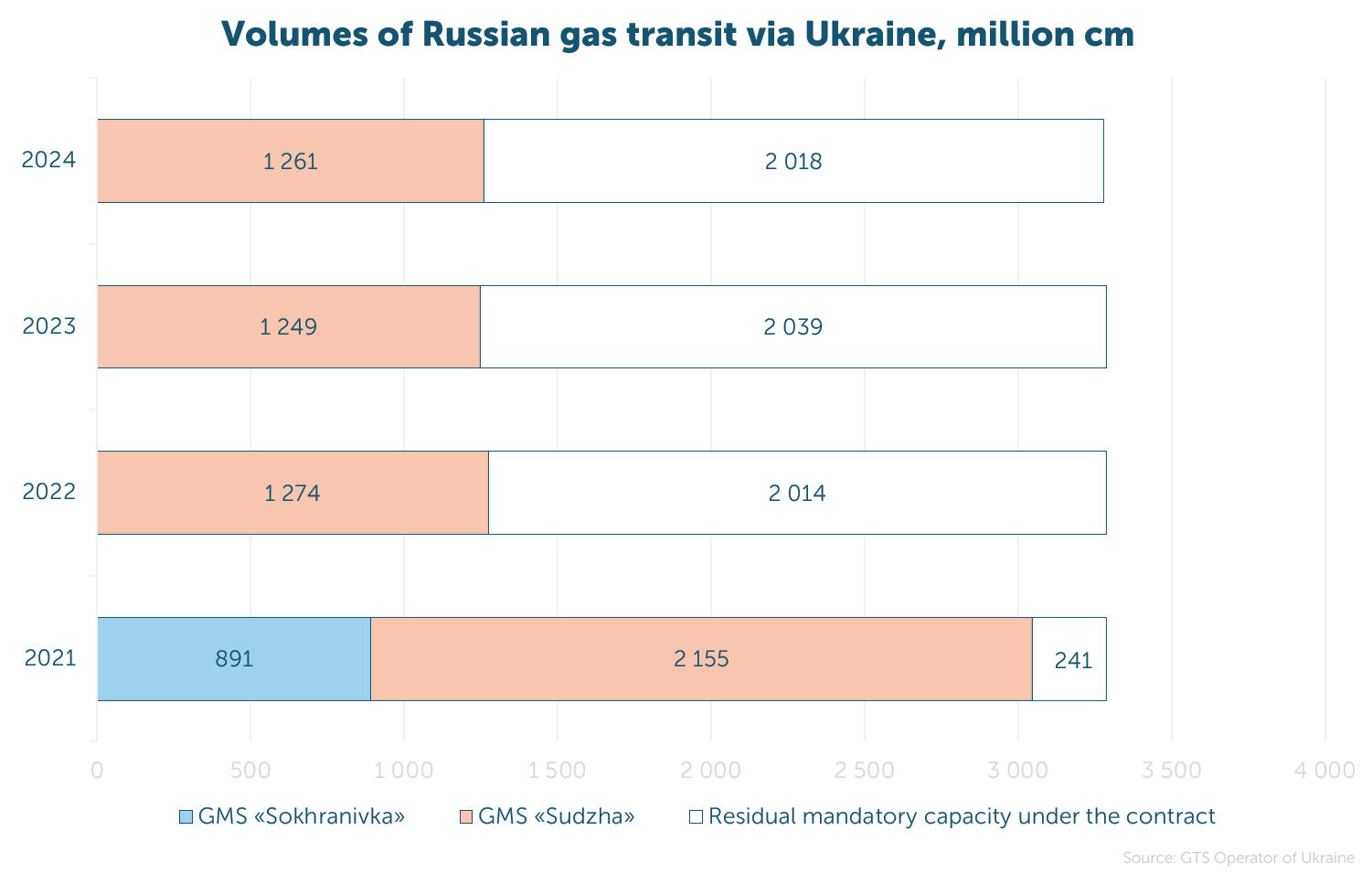

In November, Ukraine received 243.3 million cm of gas, 28% less than in October. Of this volume, 89% was transported from Hungary, and 11% from Moldova.

Gazprom transmitted 1.26 bcm in November, accounting for 38% of the contracted volume. This is 1% more than in 2023 but 59% less compared to the same period in 2021.

The total transit volume for the 11 months amounted to 14.17 bcm, 6% higher than last year.