The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

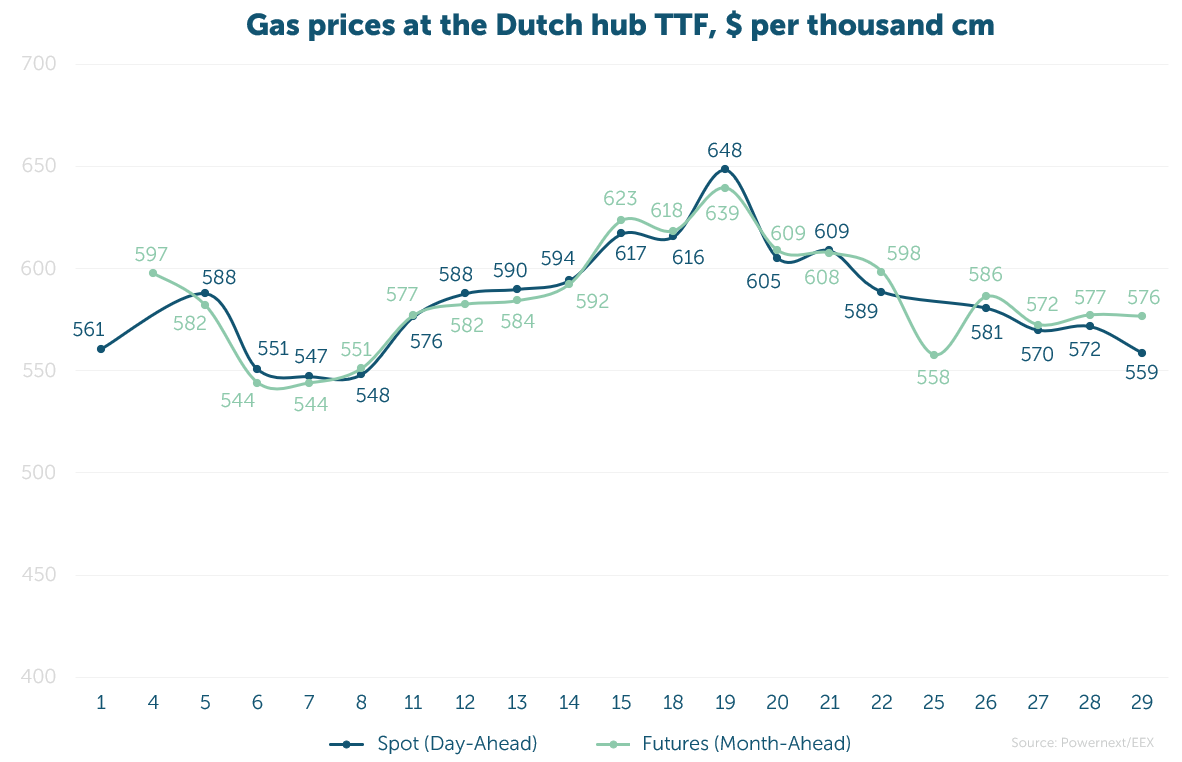

The average spot price stood at 47.207 EUR/MWh ($584, or UAH 25 750 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last trading day, was 47.335 EUR/MWh ($586, or UAH 25 820 per thcm).

Over the month, spot market prices increased by 5.2%, while futures rose by 5.9%. The price differential between these derivatives amounted to 0.3%, and volatility reached 20%.

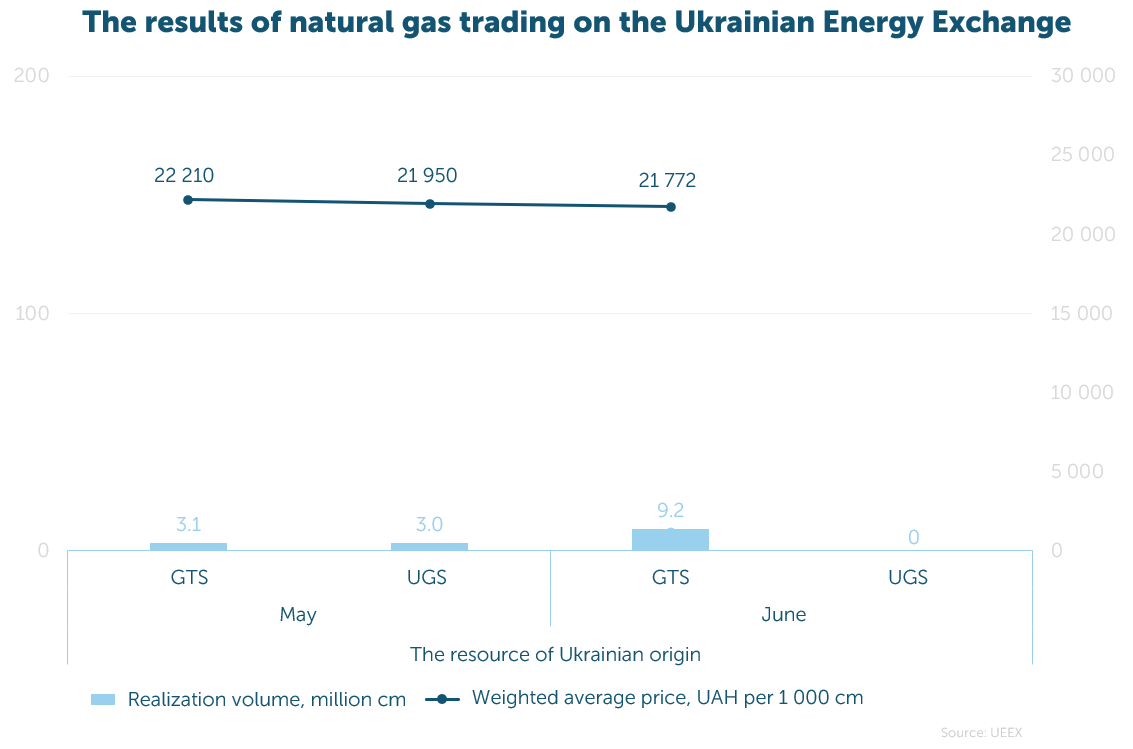

In May, 15.2 mcm of gas was traded on the exchange at a volume-weighted average price of UAH 21 895 per thcm, VAT excl. All of the sold volume was Ukrainian origin gas.

Successful sellers included Naftogaz Trading (7%), as well as other trading participants (93%). Buyers included GTSOU, which purchased gas for electricity generation purposes (56%), Ukrzaliznytsia (25%), MTM (7%), Cherkasyteplokomunenergo (4%), Naftogaz Trading (1%), and Energo Zbut Trans (1%).

In total, 149.1 mcm of gas was sold on the UEEX in 2026, excluding VOG, of which 139.8 – domestic, and 9.3 – imported.

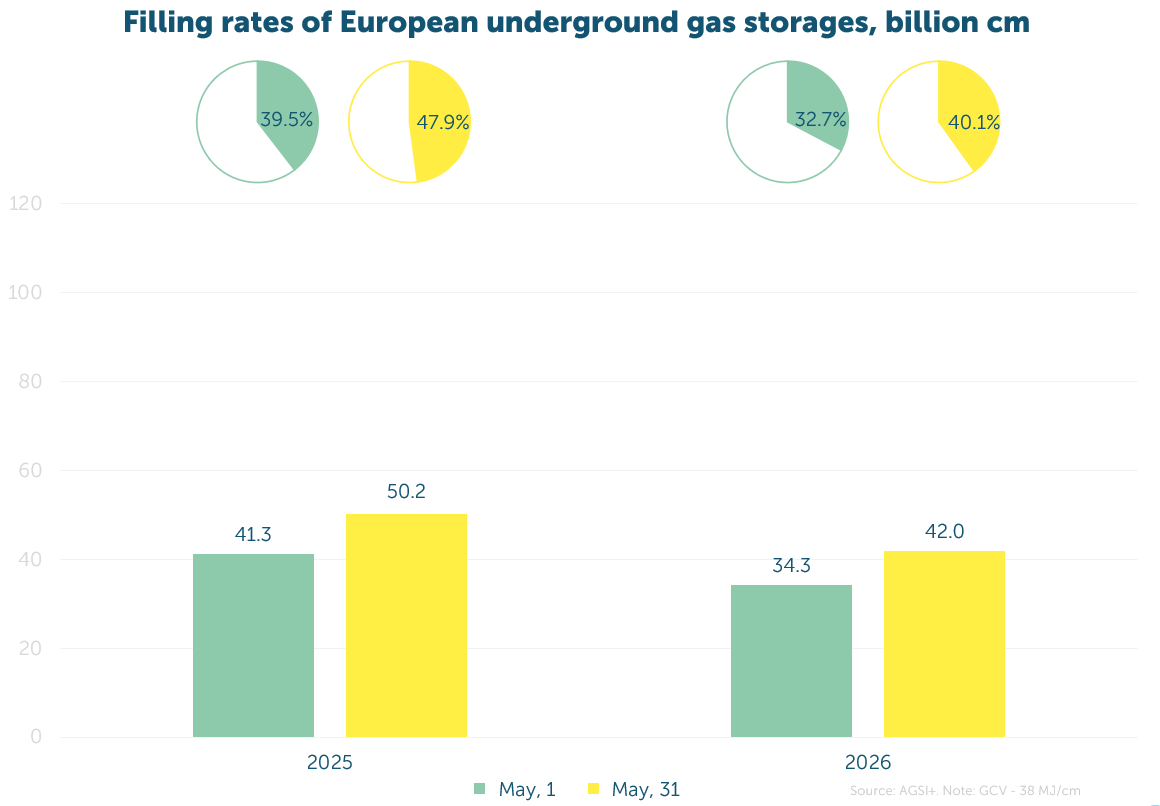

In May, Europe faced not so much a physical gas shortage as a situation where injecting gas into UGS facilities was commercially unattractive. Prices remained high, while the seasonal price spread was too narrow for businesses to buy gas “for storage” on a large scale. As a result, injection rates remained restrained, while the market was nervously assessing whether there would be enough time/supply to prepare for winter.

Against this backdrop, Equinor publicly warned that Europe could struggle to reach even 80% storage fullness by winter, while in the event of serious disruptions in LNG logistics, stocks could approach a critically low level.