The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

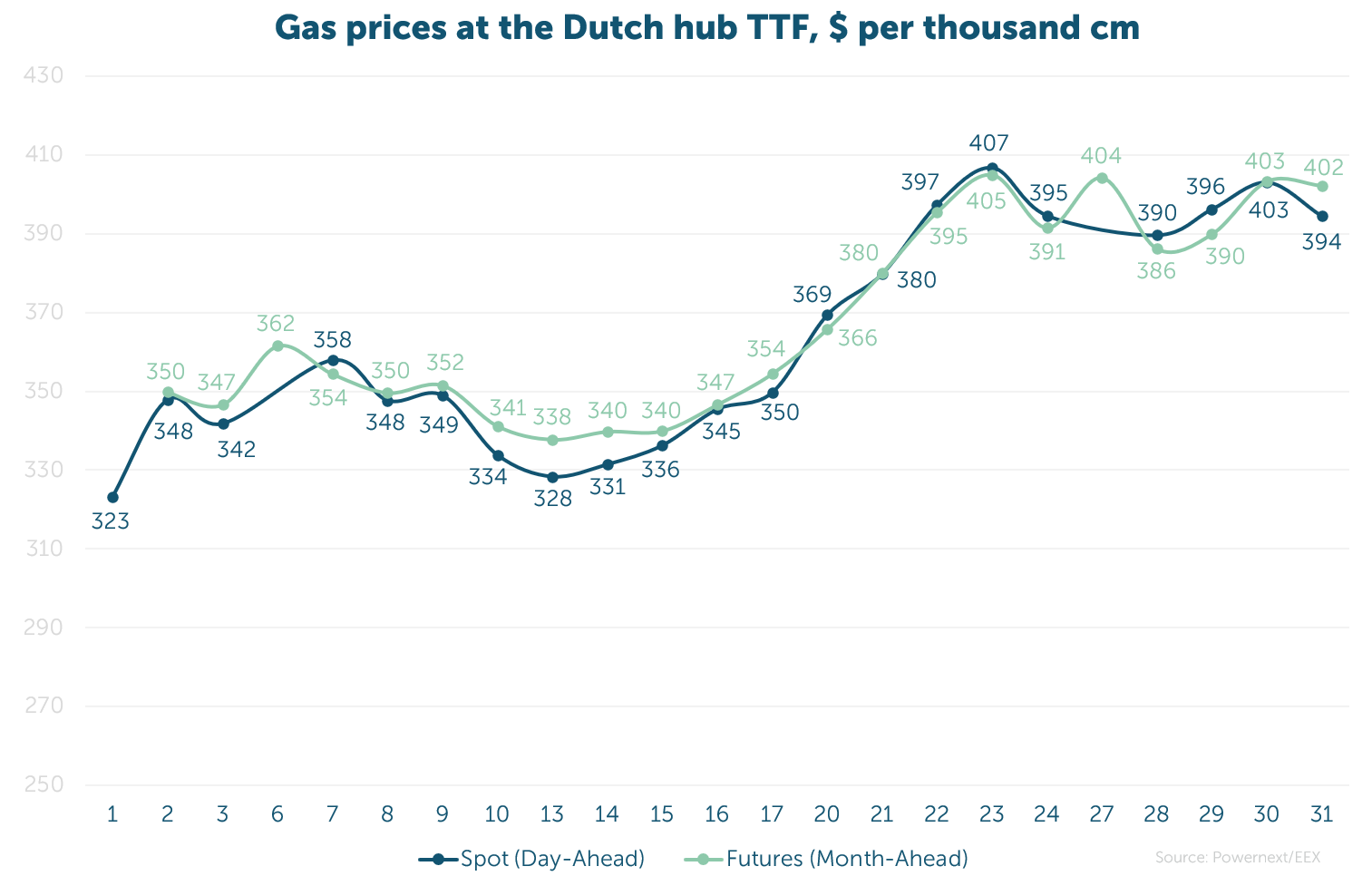

The average spot price was 31.700 EUR/MWh ($363, or UAH 14 407 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, was 31.990 EUR/MWh ($366, or UAH 14 539 per thcm).

An increase of 8.8% and 10.4% was recorded in the spot and futures markets, respectively. The price difference among these derivatives was 0.9%.

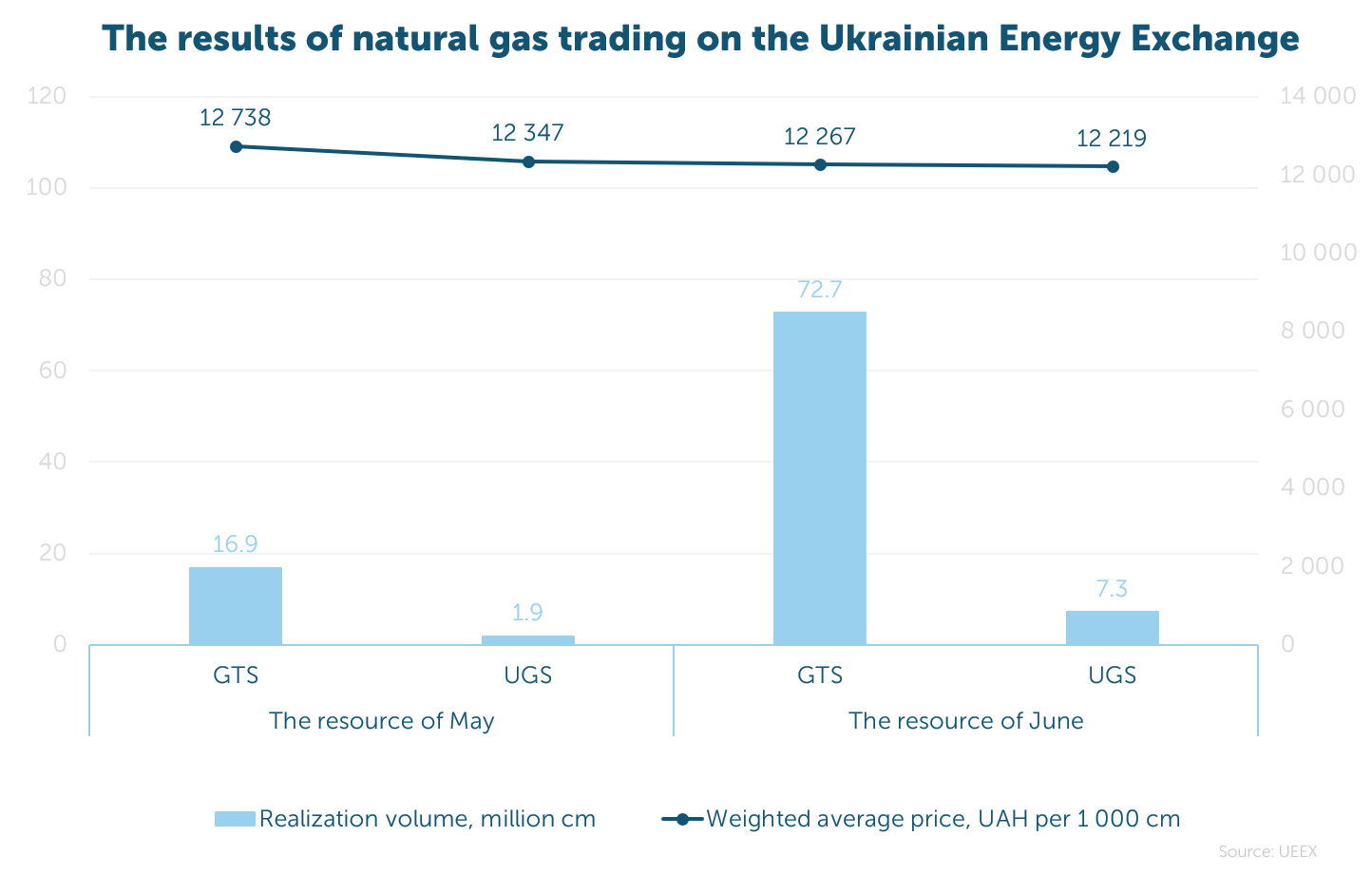

In May, 98.8 million cm of gas was sold on the exchange at a weighted average price of UAH 12 346 per thcm (excluding VAT, under all payment terms in the GTS and UGS). Notably, 91% of the volume was traded in the GTS and 9% in the UGS.

The most active trading participants throughout the month were Ukrnafta and the GTSOU, accounting for over 92% of the total volume, or 91.1 million cm.

Over the last 17 months, 1.841 bcm of natural gas has been successfully sold on the UEEX (excluding GMU).

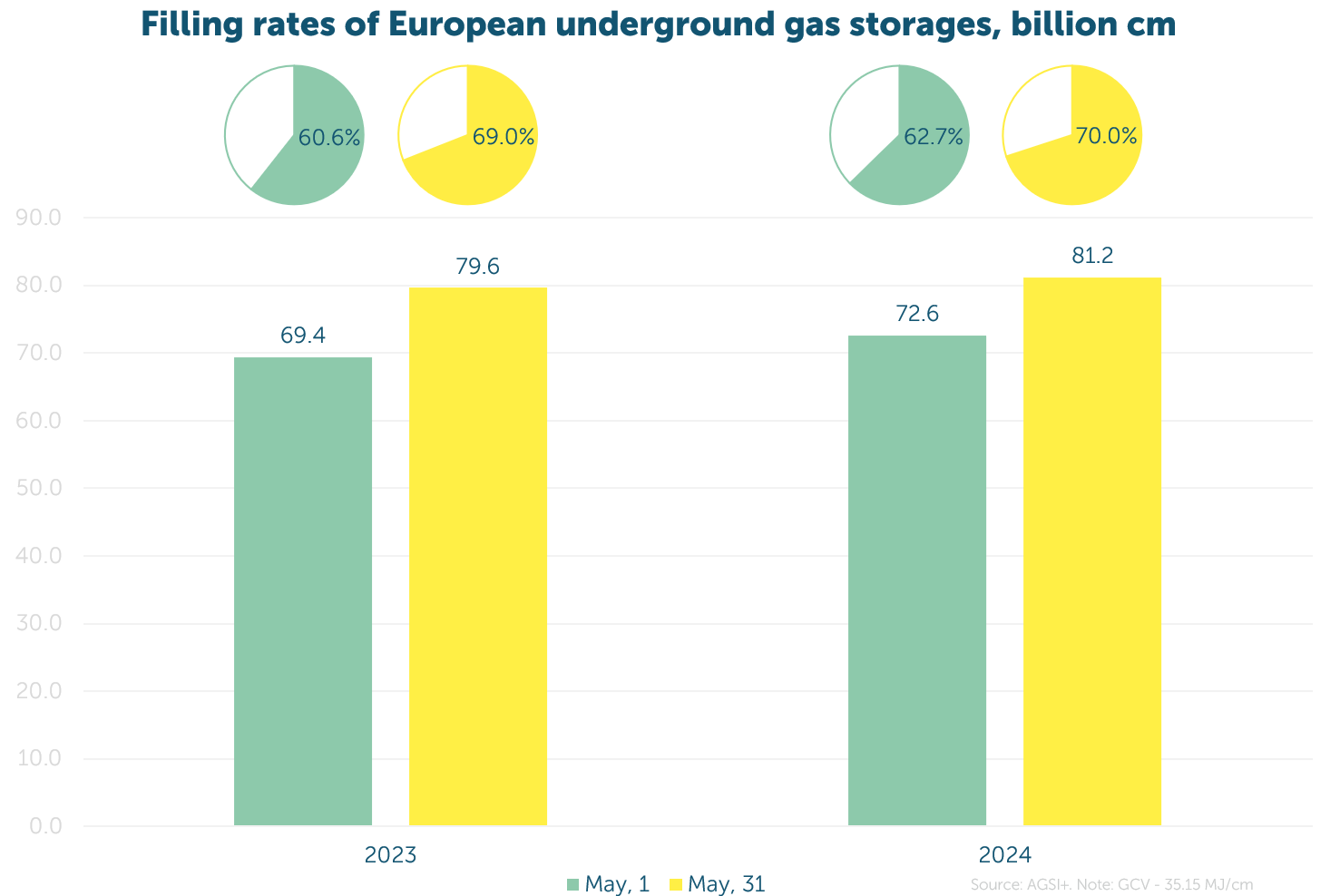

The fill levels of European UGSs remain a foundation of market stability. At the end of May, storages held 2% more gas than the previous year.

At the same time, the Vertical Corridor initiative is gaining momentum, offering the region an expansion of gas supply sources through new floating regasification and storage units, as well as resource transportation from south to north.

In July, the GTS Operator of Ukraine and its partners will conduct binding auctions for new (increased) capacity.

Since the beginning of the month, 151.9 million cm of gas has been delivered to Ukraine, which is 2.5 times more than in April. 100% of the resource was transported from Hungary.

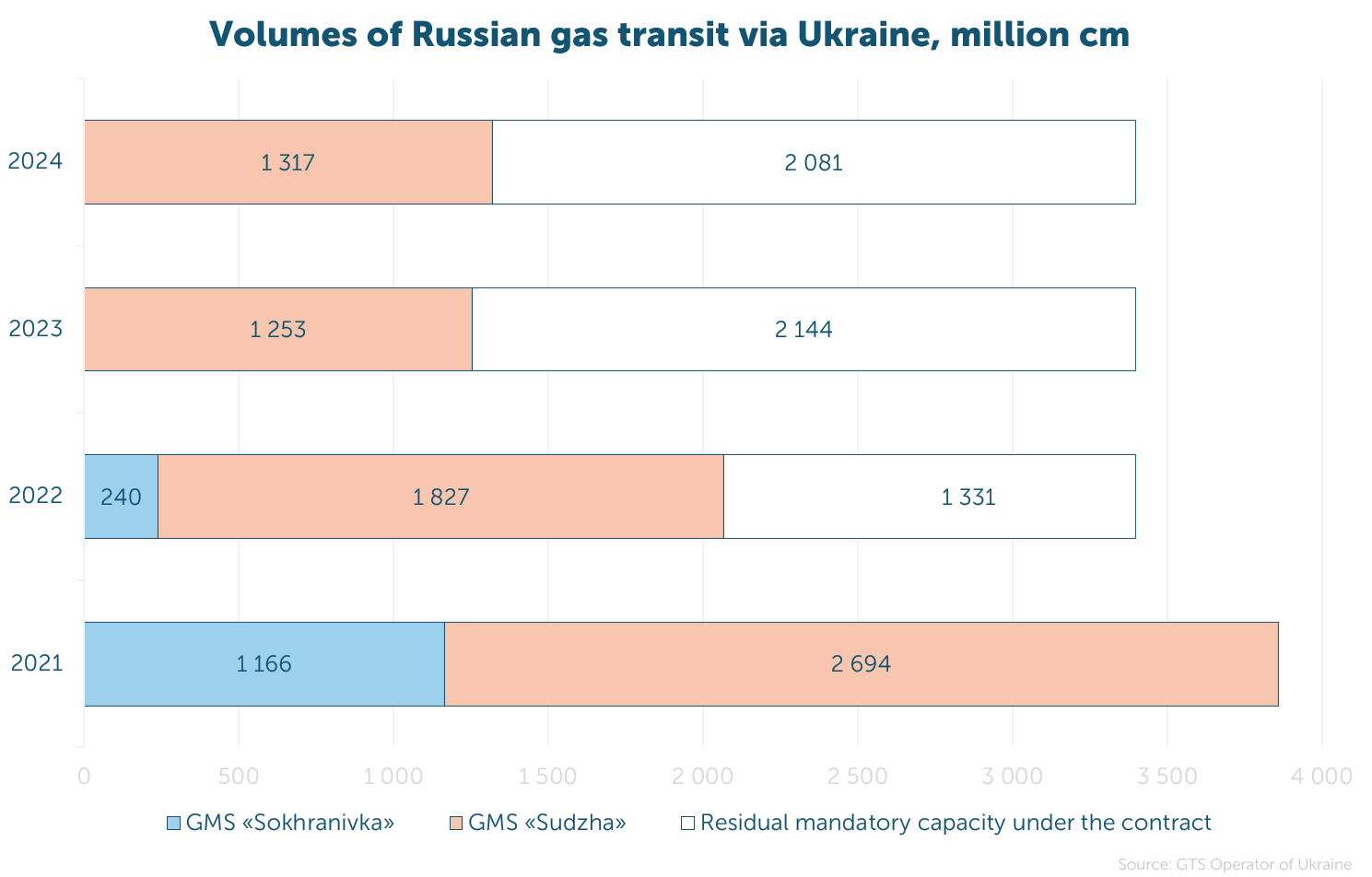

The transit volume in January-May 2024 amounted to 6.4 bcm of gas, which is 13% more compared to the same period last year.

In May, Gazprom transported 1.31 bcm, which is only 39% of the contracted volume. This is 5% more than last year, but 36% less than in 2022 and 66% less than in 2021.