The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

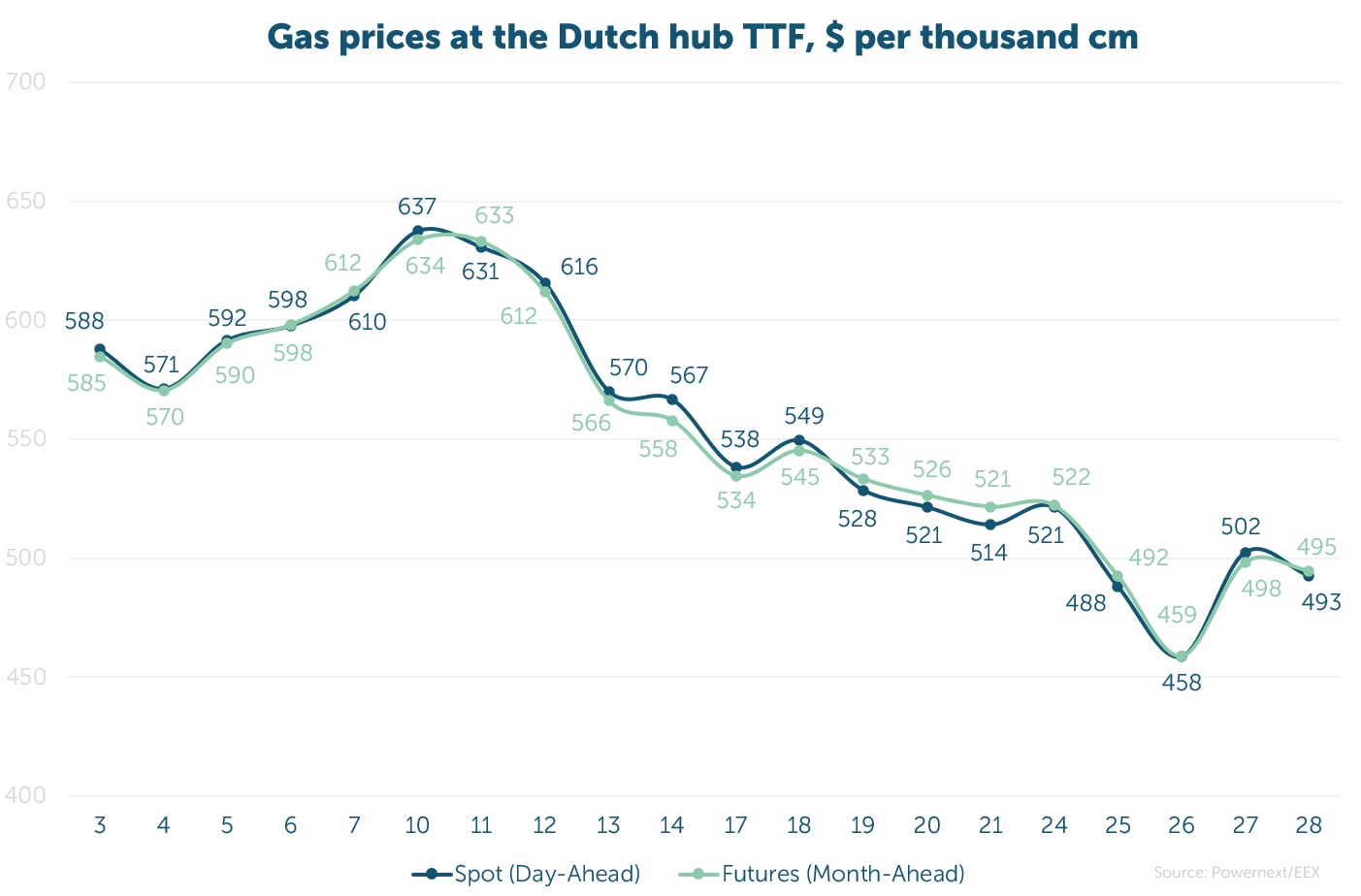

The average spot price stood at 50.320 EUR/MWh ($555 or UAH 23 127 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, was 50.571 EUR/MWh ($526, or UAH 23 242 per thcm).

Over the month, the spot market price rose by 3.5%, while the futures increased by 5.5%. The difference between these derivatives stood at 0.5%.

In February, a total of 121.9 million cm were traded on the exchange. Of this volume, 20.7 million cm of Ukrainian gas were sold at a weighted average price of UAH 17 675 (exclud-ing VAT), and 101.1 million cm of imported gas at UAH 29 662.

Ukraine’s UGS Operator ensured an 83% success rate in these trades by purchasing imported gas resources for delivery in February–March and March–April 2025.

Overall, since 2022, 3.544 bcm have been sold on the Ukrainian Energy Exchange (excluding GMU).

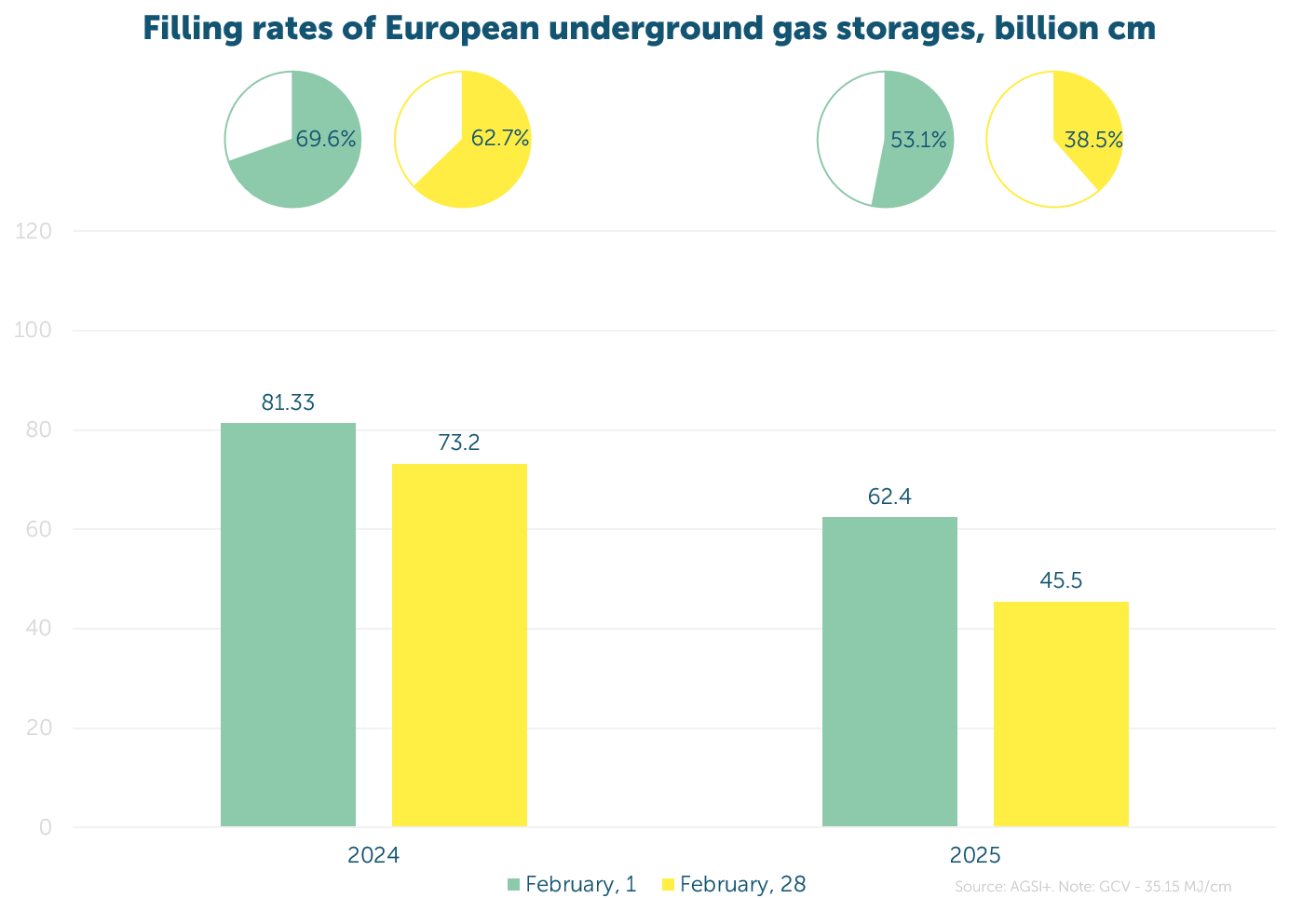

In February, gas withdrawals from European storages reached their highest level in the past seven years. Over the course of the month, inventories declined by 14.6%.

The main reasons behind this included cold weather during the first half of the month, as well as a low share of wind energy in the generation mix.

To prevent sharp market fluctuations during the next injection season, European countries are increasingly discussing adjustments to their gas storage obligations, expanding cooperation in LNG, and scaling up the share of RES.

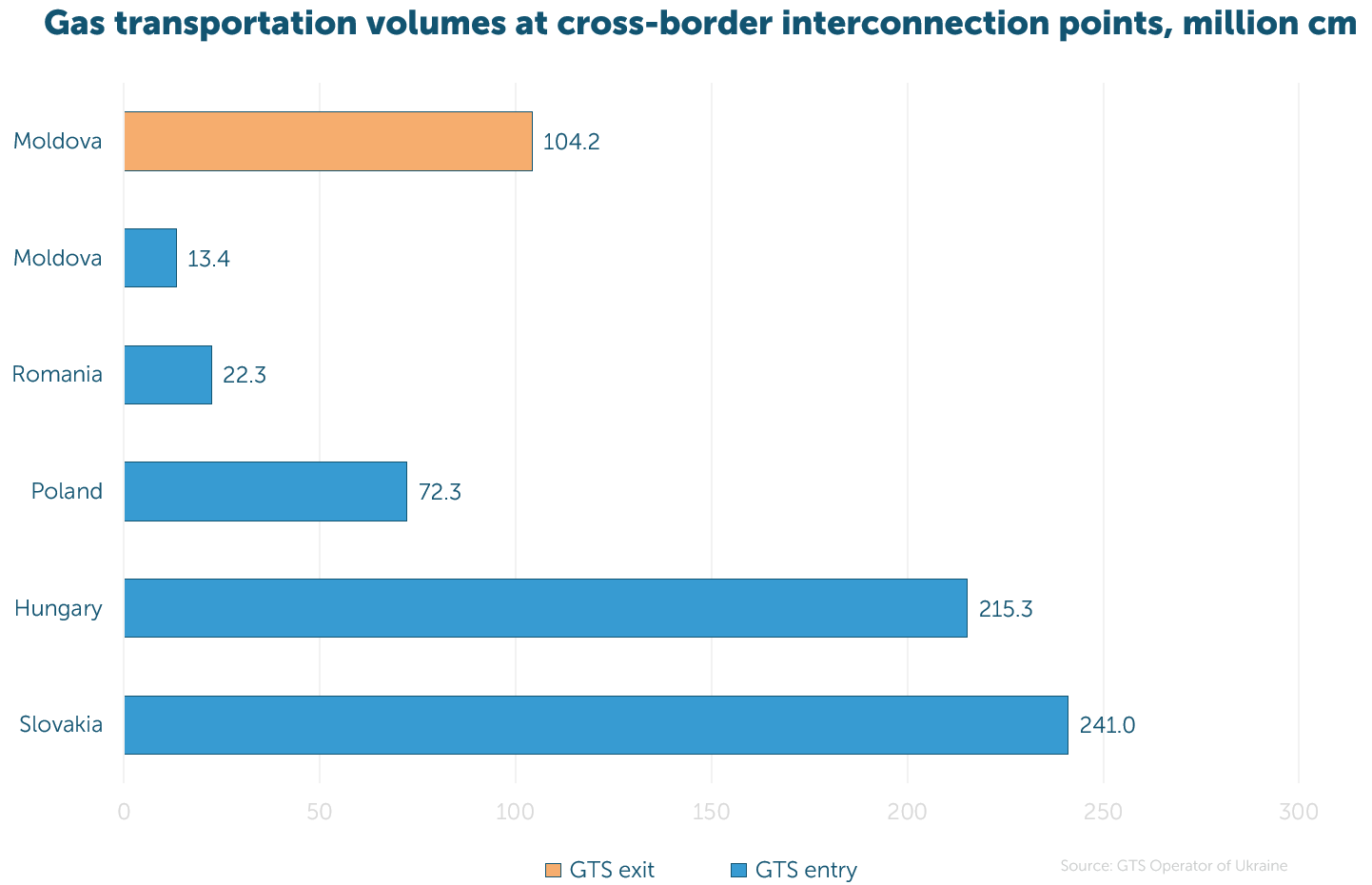

Since the beginning of the month, 564.3 million cm have been transported to Ukraine, which is 6.5 times more than the previous month. Of this volume, 43% came from Slovakia, 38% from Hungary, 13% from Poland, 4% from Romania, and 2% from Moldova.

Due to large-scale attacks by the aggressor on gas production facilities — both state-owned and private — Ukraine has been compelled to increase its imports of natural gas.

Despite all the challenges, Ukraine’s GTS continues to operate successfully without any transit of Russian gas.