The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

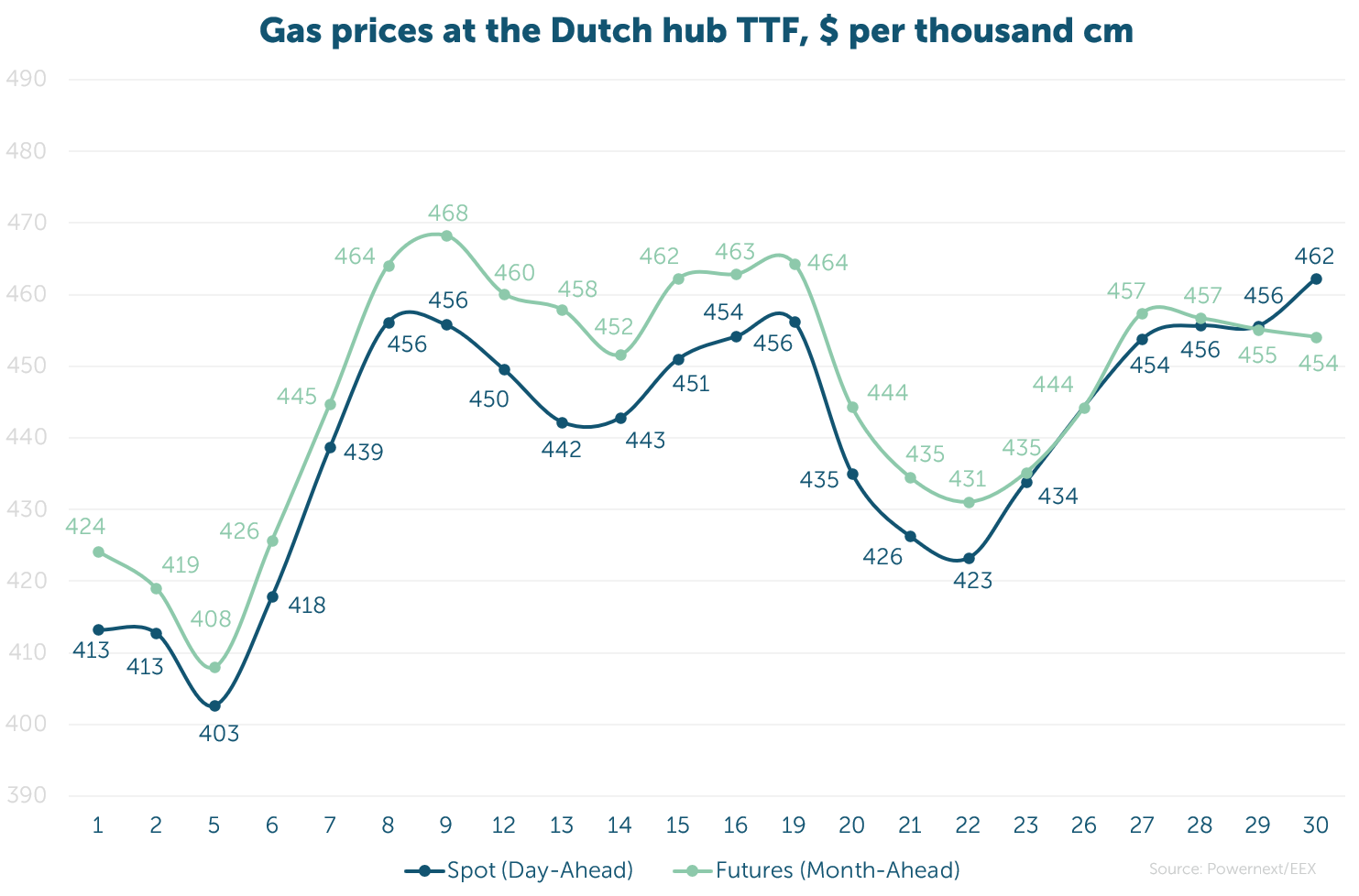

The average spot price was 37.743 EUR/MWh ($440, or UAH 18 120 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, was 38.299 EUR/MWh ($446, or UAH 18 387 per thcm).

The spot market price increased by 17.2%, while the futures market price grew by 18.2%. The price difference between these indicators amounted to 1.5%.

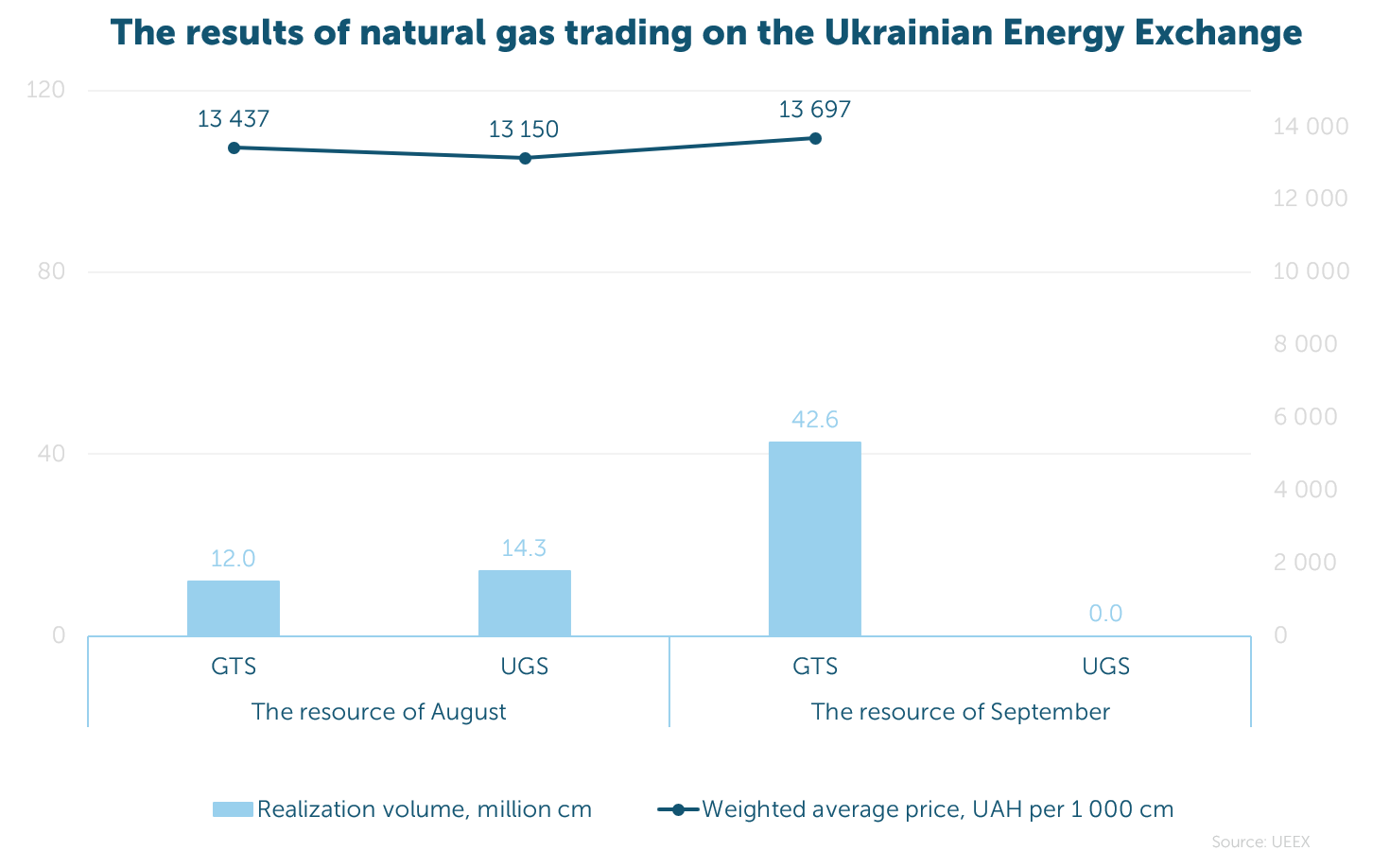

During the month, 68.9 million cm of gas were sold on the exchange at an average price of UAH 13 538 per thcm (net of VAT, under all payment terms in the GTS and UGS). 79% of the resource was sold/purchased in the GTS, and 21% in the UGS.

The most active participant in the trading was Ukrnafta, which sold 62.8 million cm, or 91% of the total volume.

Over the last 20 months, 2.335 bcm of natural gas have been successfully sold on the UEEX (excluding GMU).

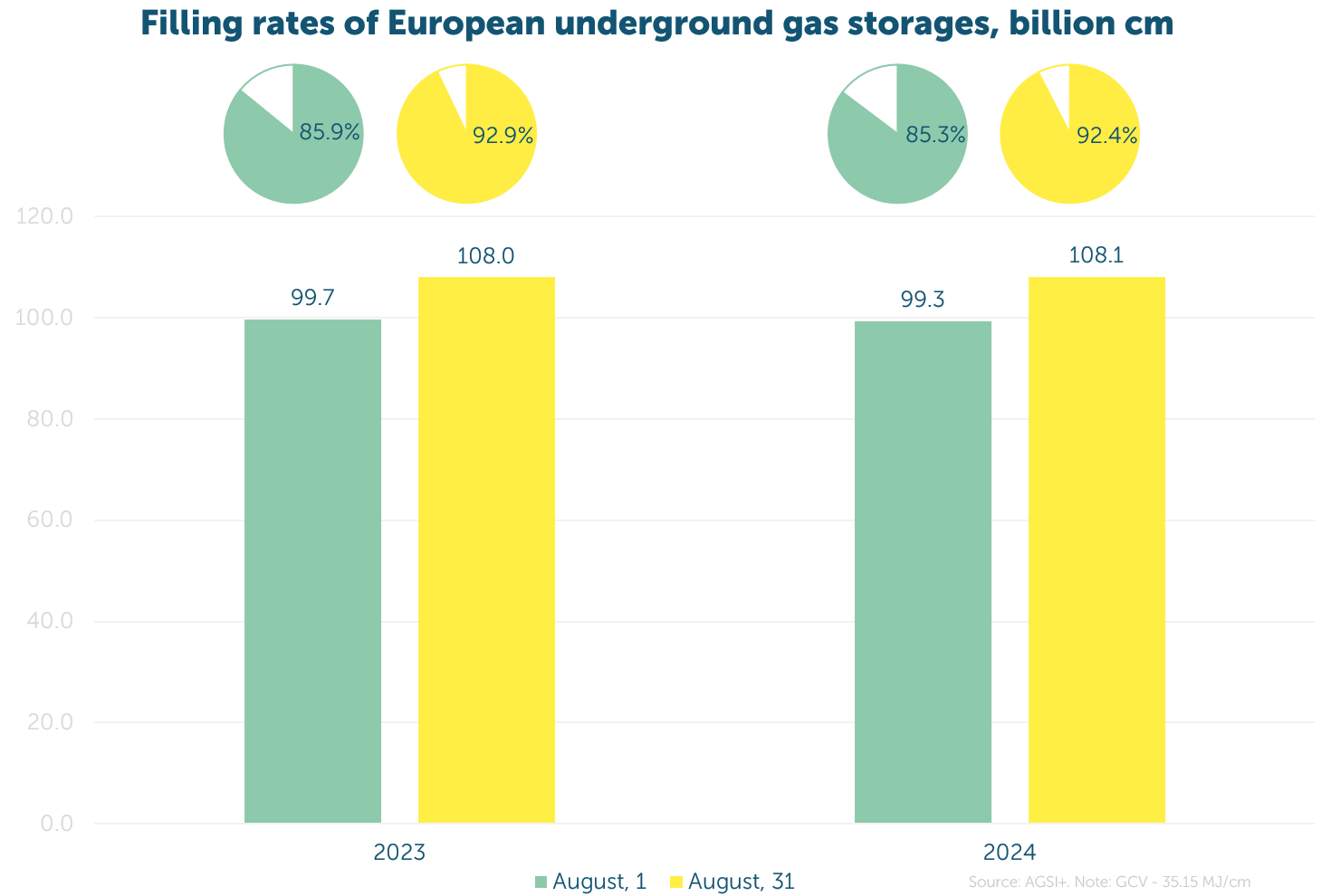

In one month, European gas storages were filled by 7.1%. By the last month of summer, storage levels in some countries exceeded 100%. Considering that the share of Russian gas in the EU's imports and consumption has significantly decreased, the situation is expected to remain stable in the future.

The EU's UGS fill levels should encourage foreign traders to store resources in Ukraine. Naftogaz Group's CEO, Oleksiy Chernyshov, mentioned that Ukraine offers its gas storages to EU countries that are accumulating reserves ahead of the winter season.

In one month, Ukraine received 138.6 million cm of gas, which is 60% more than in July. The vast majority of the resource, 93%, came from Hungary, with 7% from Romania.

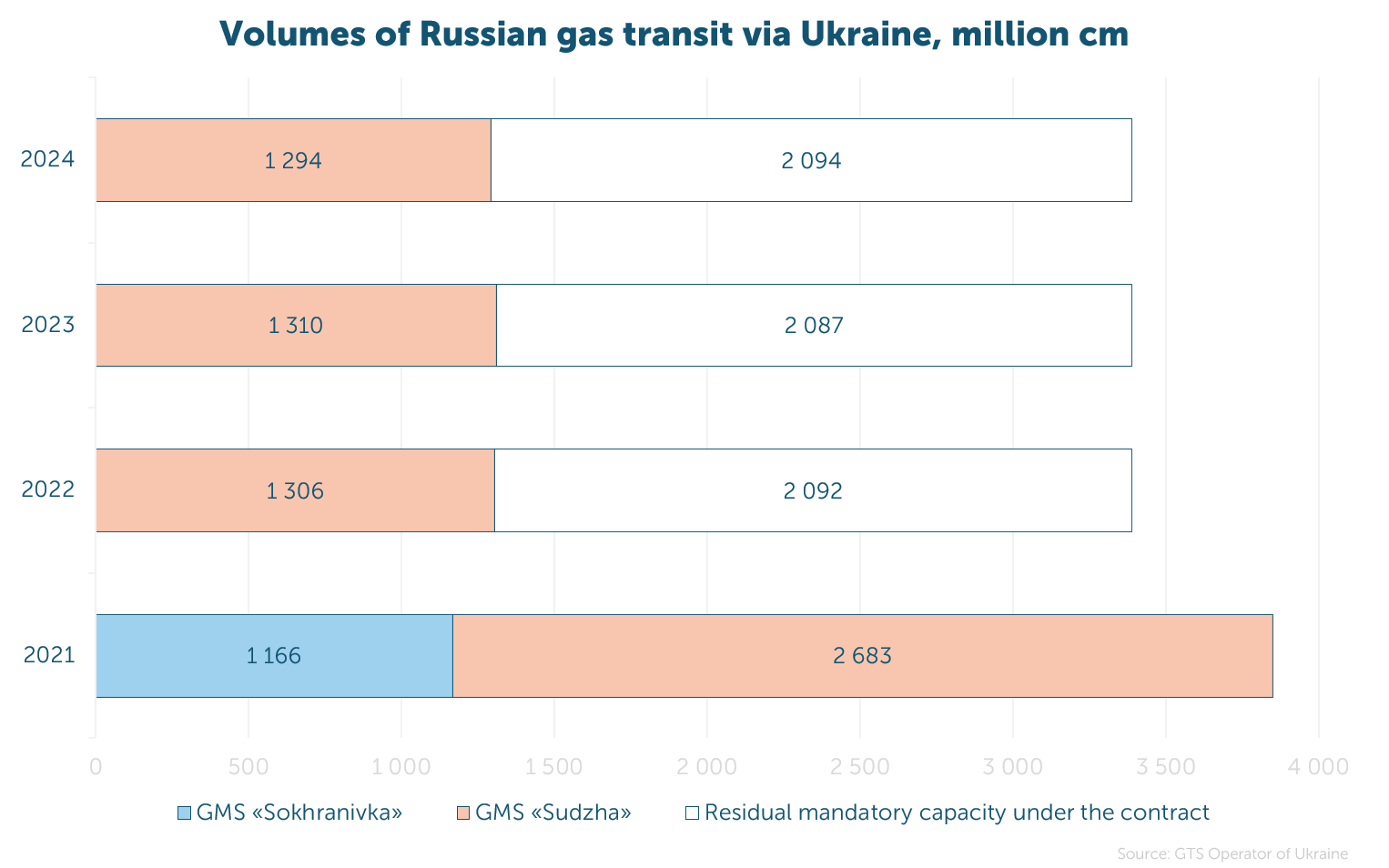

In August, Gazprom transported 1.29 bcm, or 38% of the contracted volume. This is 1% more than in 2023 and 2022, but 66% less compared to the same period in 2021.

The total transit volume for the first 8 months was 10.3 bcm, which is 8% more than last year.