The Association of Gas Producers of Ukraine presents the current information on the Ukrainian and European gas markets.

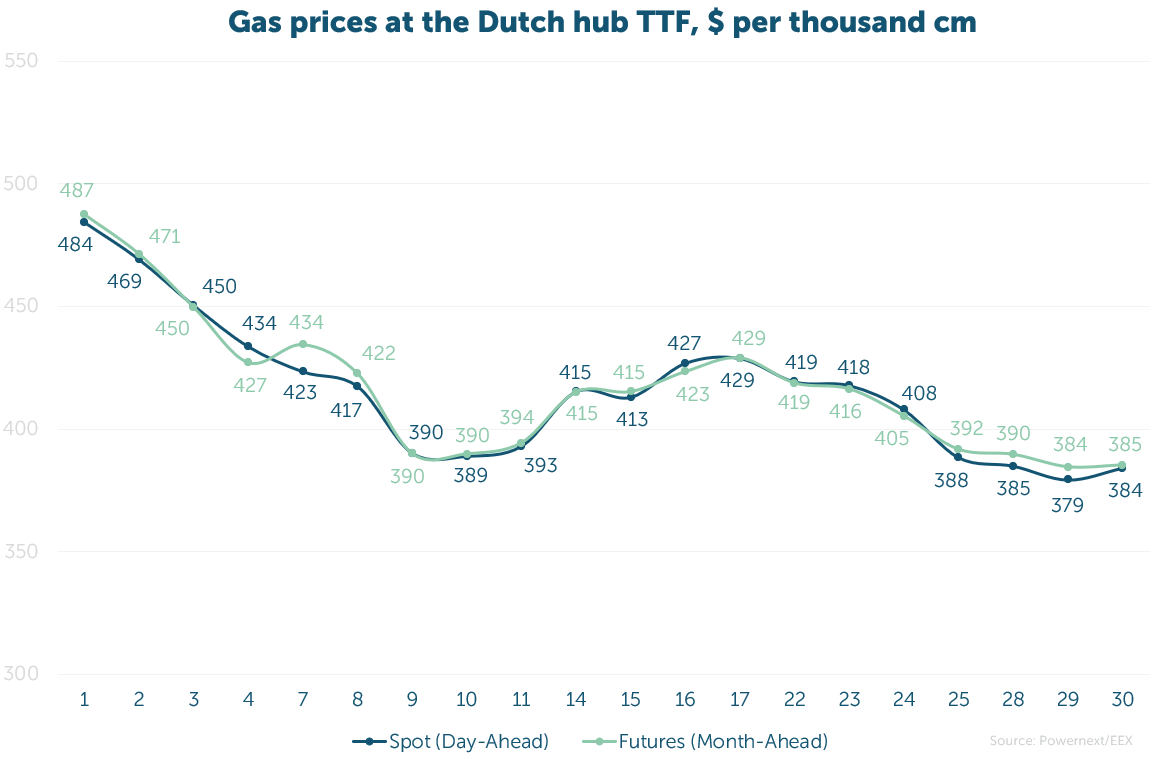

The average spot price stood at 35.089 EUR/MWh ($417, or UAH 17 272 per thcm).

The average futures price at the TTF hub (Month-Ahead), excluding the last day, amounted to 35.357 EUR/MWh ($420 or UAH 17 404 per thcm).

Throughout the month, gas prices on both the spot and futures markets in Europe dropped by 15%. The price spread between these derivatives was 0.8%, while volatility ranged by 33-34%.

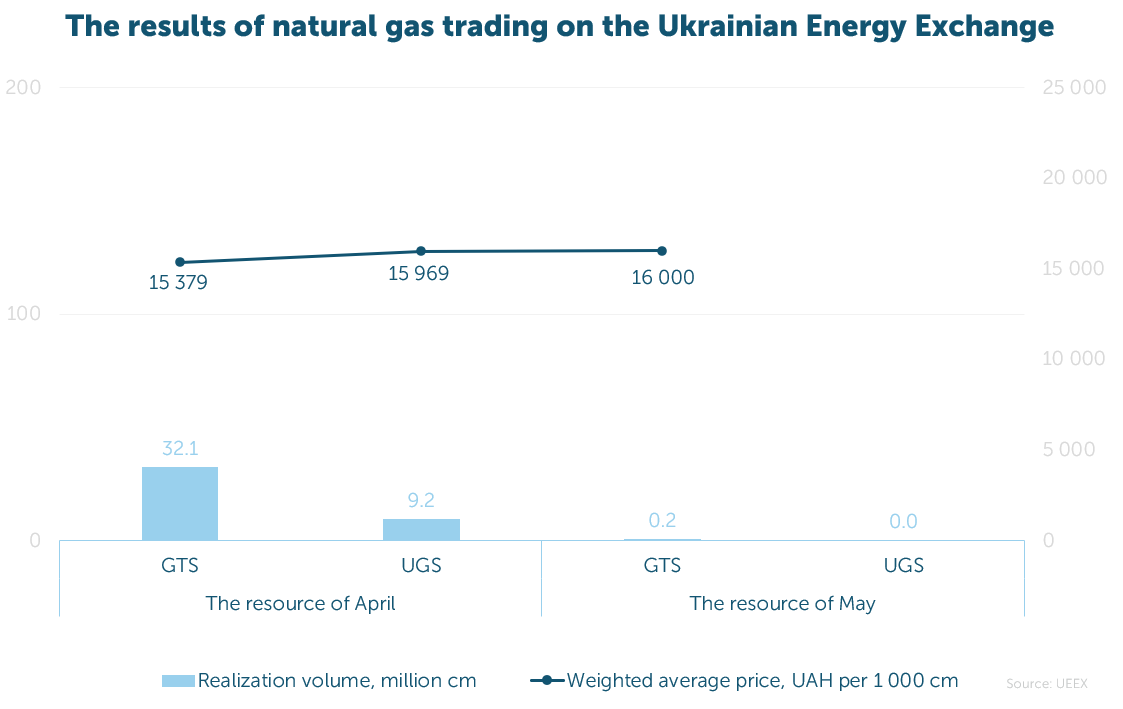

In April, 41.5 million cm of Ukrainian gas were traded on the exchange at a weighted average price of UAH 15 525 per thcm (net of VAT).

The most active buyers during the month were the GTSOU (52%) and the Naftogaz Group (17%). Among the sellers were Ukrnaftoburinnia – 10.45 million cm (25%) and ERU – 2.0 million cm (5%).

Overall, since 2022, a total of 3.652 bcm have been sold on the Ukrainian Energy Exchange (excluding GMU).

To prepare for the upcoming winter, analysts estimate that Europe may need up to 250 additional LNG cargoes (approximately 26 bcm), worth at least $11 billion.

According to Jason Feer, Global Head of Business Intelligence at energy and shipping brokerage Poten & Partners: «Europe will have to buy fairly aggressively this spring and summer to refill inventories».

Experience from previous seasons suggests that the region will need to pay a premium to attract cargoes, competing with buyers in Asia.

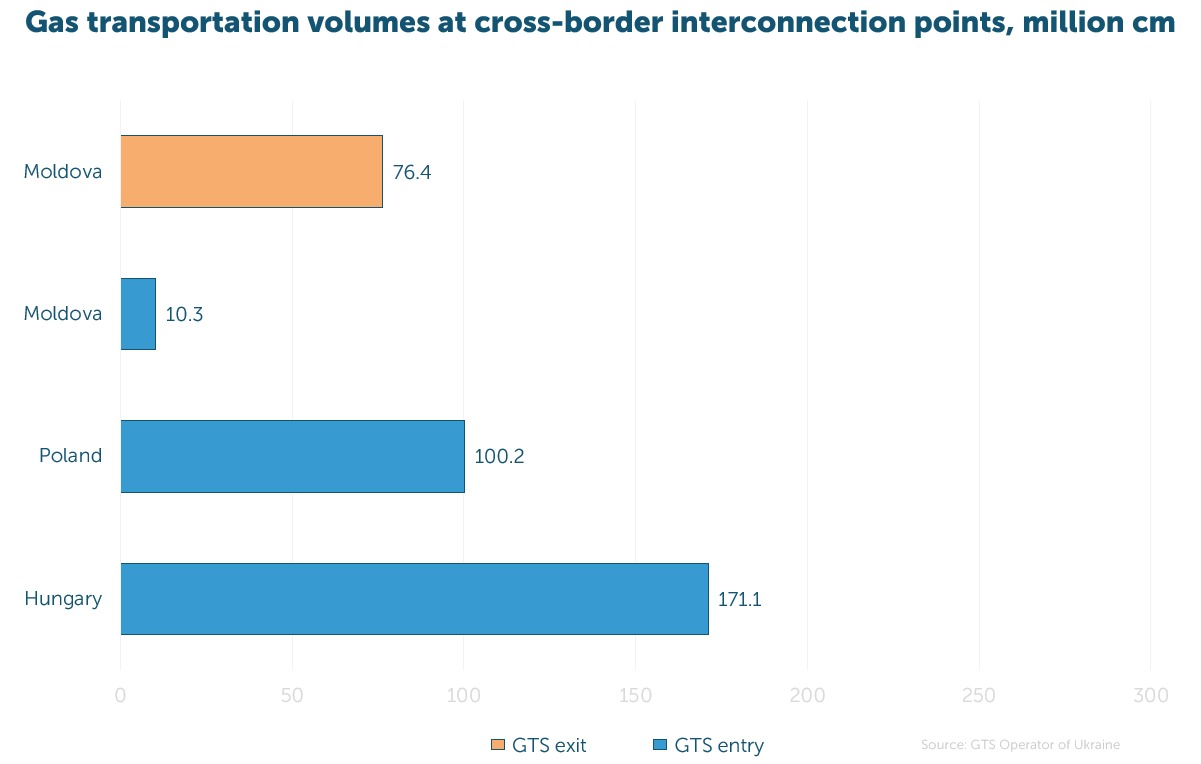

In April, 281.6 million cm of gas were transported to Ukraine, 12% less than the previous month. Of this volume, 61% came from Hungary, 36% from Poland, and 4% from Moldova.

The convergence of Ukrainian and European gas prices is expected to support increased imports, stimulating trader activity and enabling more efficient use of gas storages.

Between January and April, 1.24 bcm of gas were transported from Europe to Ukraine, while 0.27 bcm were shipped from the Ukrainian GTS.