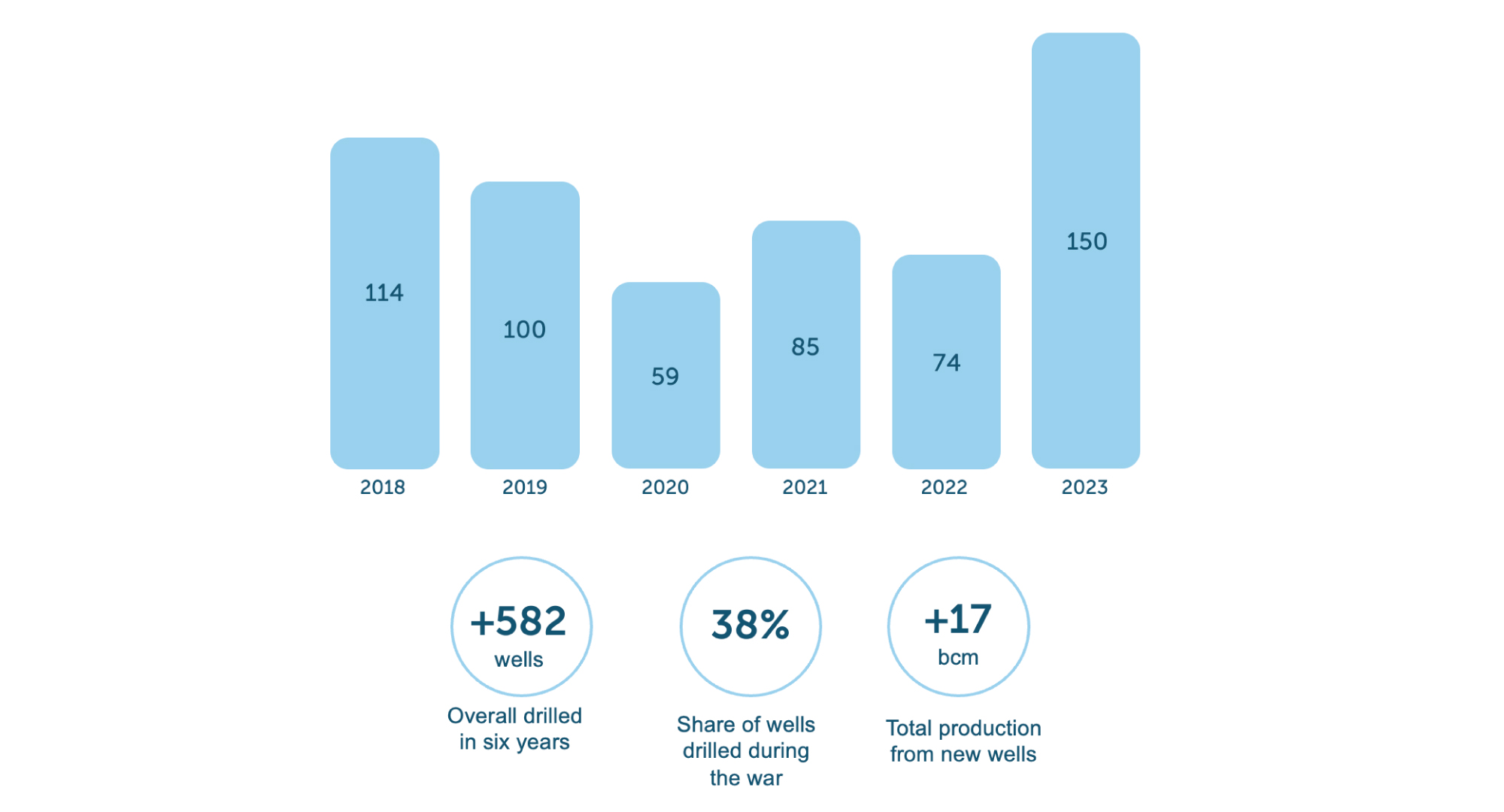

This is the highest number since 2018 when incentive taxation was implemented.

Last year, gas producers increased the number of new wells by 32% compared to 2018 and doubled the volumes compared to the first year of Russian aggression.

It's important to note that the share of wells drilled in Ukraine during the full-scale war accounts for more than a third of the total number over the last six years.

In 2023, an average of 42 drilling rigs were in operation on the Ukrainian market – more than half of the total European figures. This was despite all the war risks, regular shelling, logistical challenges with equipment, and the absence of international service companies.

The increase in sector activity was due to the successful actions of the Ukrainian army at the front and preserved tax incentives.

It's no secret that the largest fields in Ukraine are depleted by more than 80%, having been developed since the 1960s and 1970s. Natural decline at old wells averages 15% per year. Therefore, the only chance for companies to maintain and increase gas production is to drill new wells.

The main factors for producers in making an investment decision on drilling are geology, cost of work, availability of equipment and technology, and, most importantly – the fiscal system in place in the country. However, even this does not guarantee success, as a well might be "dry". In the case of successful drilling, the obtained flow rates depend on the region of production, the age of the fields, and the depth of the deposits. Wells up to 2 km deep in the western regions will be cheaper but yield less gas – 10-50 thcm per day, while the flow rate of deeper and significantly more expensive wells in the east can be 200-300 thcm per day.